Plant Construction Survey

2018 Plant Construction Survey: Rising Rate of Food & Beverage Plant Renovations/Expansions

Many food & beverage processors are renovating/expanding their existing plants to meet FSMA and consumer demands.

You’ve looked at the options. You own your site. Sure, the building is a little “mature,” but with some TLC and the help of your A&E/C firm, you can renovate the building, so it will meet food safety regulations, building codes, EPA and zoning laws—and even your municipality’s wastewater treatment requirements. Renovating your food or beverage plant can be done in stages, so as not to upset production. There’s even room to expand the building, and your design-build firm has done all the risk assessments, verifying that renovating and expanding are possible. Now, all that’s left, is what may be the toughest question: What will your business look like five, 10 or 20 years from now?

While the bulk of FSMA-based food and beverage processors have done their homework in preparing their plants, not only to meet FSMA regulations, but also GFSI certifications and customer requirements, some are still weighing many considerations to see if it makes sense to stay put and fix up or build at a new site altogether.

Article Index:

Manufacturers are more proactive now, says Mark Galbraith, co-owner of Galbraith Pre-Design, Inc. Processors have come to know what to expect during inspections and what they need to do to be in compliance. However, processors do not necessarily know what design, materials and methods it takes to construct a facility that will be in compliance and easier to maintain, so it stays in compliance; it is the role of the A&E/C to provide the education and resources to help get a processor’s facility into compliance.

Processors that find it cost prohibitive to meet certification requirements with older plants instead look at new facilities vs. modifications, according to Jack Michler, ESI Group USA regional manager.

“We are seeing companies bringing manufacturing operations back in house to offer more product flexibility and control of new product offerings based on trends for artisanal, organic and locally sourced products, especially for the growing meal kit market,” he says.

“We are still seeing a lot of renovations taking place, as it becomes increasingly difficult for the oldest of plants not only to meet federal regulations, such as FSMA, but to keep up with demand and compete with modern plants,” says Mike Follmer, RA, Hixson Architecture & Engineering vice president & senior project architect.

Processors are finding that when these outdated facilities can no longer be fixed with make-do solutions, they must either choose to consolidate production from older facilities into new plants or completely modernize existing plants.

Looking for quick answers on food safety topics?

Try Ask FSM, our new smart AI search tool.

Ask FSM →

Staying put and modernizing can have its advantages. The retrofitting of existing buildings and their specifications seems to be a trend—more so than new greenfield construction, says Jed Dearduff, The Austin Company corporate director, baking and snack. Why? The need to expand and be up and running sooner than new construction is the driver.

Cost consideration is also a factor, especially if you own the site outright.

“Our project load is showing expansions and repurposing projects are outpacing plant consolidation and new construction projects,” says Rick Elyar, Hansen-Rice, Inc. business manager, food and beverage. “We continue to see a trend of projects aimed at repurposing existing facilities for manufacturing more so than expanding at their current facility. By helping clients repurpose existing facilities, we are able to get them up and running in shorter timeframes and with less of a capital investment.”

Food and beverage companies are increasingly considering retrofitting existing facilities to get products to market more quickly, says Todd Allsup, Stellar vice president, sales, food group. Speed to market is becoming more important in today’s market, and greenfield projects may not always suit a company’s strategic schedule for launching a particular product. Of course, retrofitting comes with its own set of challenges. Owners must truly understand what they’re investing in when looking at existing facilities to ensure they’re not diving head first into a money pit, adds Allsup.

In this graph, the blue bars

represent the ratio of renovations

and expansions compared

to new projects. For the last six

years, the ratio has increased, and

in 2017, about three out of four

projects reported were expansions

and/or renovations. The red

trace shows the total number of

projects reported each year.

“As far as upgrading old plants, generally that is [done on] a case-by-case basis,” says Keith Perkey, Haskell vice president—food and beverage. “The answer depends on a risk analysis for the product. We are seeing some trending towards greenfield facilities to replace old plants that are out of compliance and inefficient.”

A look at the numbers

The numbers derived from FE’s 2018 Annual Plant Construction Survey certainly reflect the above discussion—that is, the number of renovations and expansions in 2017 far surpasses that of new construction by a ratio of 2.81:1. Not only that, the ratio of renovations and expansions to new greenfield projects is the highest it’s been in the 12 years I’ve been doing this survey and is the highest of the last five years (2013 to 2017), accounting for 73.8 percent of all the food and beverage projects reported in 2017. (See “Ratio of expansions to new projects” and “2014 through 2017 projects.”)

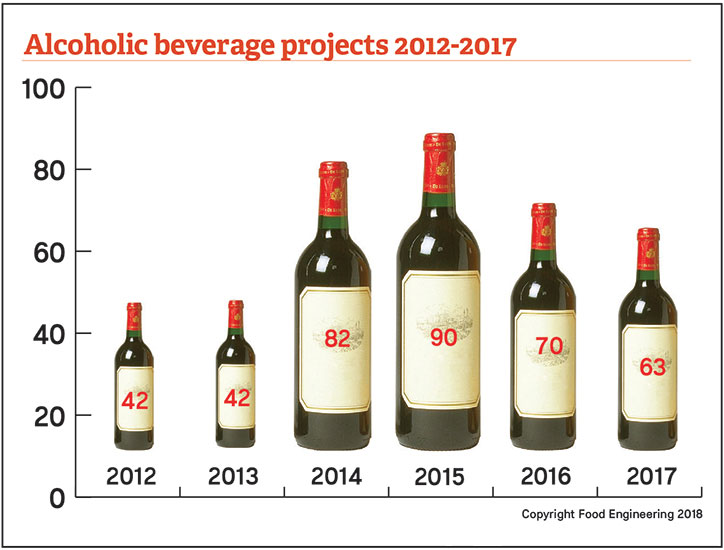

In 2017, 168 projects accounted for new or greenfield, and 472 projects included expansions and/or renovations. Out of the total of 640 reportable projects in 2017, 85 were warehousing or distribution projects (including alcoholic beverages) and included both new projects and expansions. There were 63 alcoholic beverage projects, down from 70 in 2016.

Reportable food and beverage projects are those valued at over $1 million. They have been made public by the processor, a government entity (including local or state economic development groups) or the A&E/C firms responsible for them. The survey (though the table lists “Completion Date” at the header) includes projects begun, announced by any entity or completed in 2017. If the dates listed are beyond 2017, they reflect the projected completion date for a project either announced in 2017 or currently under way. Keep in mind, some projects can be announced, then dropped at the last minute for any number of reasons, e.g., legal problems, lack of expected funding, site issues, changing needs, politics, etc. In the table, “D/W” refers to distribution/warehouse, and “DC” refers to distribution center.

While the total number (640) of projects in 2017 dropped by 5.7 percent from the 679 recorded in 2016, new projects (168) in 2017 dropped by almost 14 percent from the 195 recorded in 2016. Renovations and expansions (472) only dropped by 2.5 percent in 2017—from 484 projects recorded in 2016. Keep in mind that renovations or expansions might include, for example, a wastewater treatment facility added to a site to keep it operational, or additional loading/unloading capabilities.

Total projects in 2017 showed a 12.5 percent increase over the 12-year simple average of 569 projects per year. New projects in 2017 showed a 12.4 percent drop over the yearly average of 192 projects. Expansions and renovations (472) in 2017 showed a 25.3 percent increase over the 12-year average of 377 projects per year. Projects for distribution and warehouses showed a 56.9 percent increase over the 12-year simple average of 54 projects per year.

While alcoholic beverage projects declined by 10 percent, from 70 recorded in 2016 to 63 in 2017, facilities dedicated to warehousing and the distribution of any food and beverage products actually increased by 9 percent (85 projects) in 2017 (up from 78 projects recorded in 2016). Some of the increase may be attributed to those companies that are changing supply chain structures to be more resilient and competitive.

For the past six years, FE has

been tracking alcoholic

beverage producing or

warehousing facilities. Fewer

projects were listed in 2017

than 2016, and craft beer and

distillery projects accounted

for the majority.

For example, Steve Tippmann, executive vice president of the Tippmann Group, notes that his firm is seeing a demand for more plant-attached warehouses, so manufacturers can control their own distribution network rather than going to a third party.

“One trend I’ve noticed is organizations’ supply chains are optimizing processes to minimize [their] manufacturing footprint, while at the same time, maximizing manufacturing capacity within existing structures,” reports Sam Thurber, PMP, SSOE senior project manager.

What drives food manufacturing building design?

Actually, there are a multitude of different forces affecting specific areas of food innovation and processing. Jeff Johns, Shambaugh & Son senior VP, says that one driver is predicting and reacting to the wants and needs of Millennials and Gen Zers. In addition, food and beverage companies are starting to factor in e-commerce strategies and how that might affect production.

Mark Di Gino, director of business development at E.A. Bonelli + Associates, Inc. notes an interesting trend that at first seems circular—the return of end-retailers processing their own food staples. In the ‘70s and ‘80s, grocery chains like Safeway and Lucky were constantly building new process plants to manufacture their own branded goods, ranging from bread to dairy, and then, that approach was replaced with the Costco model. Now, with Walmart building its own dairy processing facility in Indiana, how long before a major retailer like Amazon/Whole Foods follows suit?

“The key is to create flexibility in design that provides [processors] with the ability to meet today’s needs, but allows for potential adaptation as markets shift,” says Forrest McNabb, Big-D Construction president. One of the most critical items is the elimination of cross-contamination of the various products being produced.

With consumers’ busy schedules, RTE meals and prepared foods are alternatives to cooking from scratch, and these have imposed new constraints on building designs.

“RTE is definitely getting bigger, which [increases] the concern for contamination protection in the building design and room finishes, says Shambaugh’s Johns.

Because of rapid product changes, plant design is more 360° in terms of potential expansion or change—in other words, being able to expand physically in all directions by not boxing in any area of the plant.

The need to produce RTE meals brings an increased interest in blast freezing, says A M King’s Stuart Jernigan, director of preconstruction. In addition, increased demand for allergen-free, non-GMO and gluten-free products is driving the design for separate processing areas for both employees and products (e.g., allergen vs. allergen-free, similar to raw vs. cooked areas). Separate employee sanitation, air and waste systems are being utilized for these areas.

“Most of these RTE processing facilities are refrigerated and wet, creating an environment highly susceptible to microbial contamination and consumer risks,” says Hansen-Rice’s Elyar.

When considering changes to a facility, Elyar suggests making food safety the starting point by launching a food safety assessment of the existing facility to determine the risks before beginning the design phase.

“The deficiencies we are finding in many older facilities can create design challenges, as we begin developing facility expansions,” adds Elyar.

Many don’t have isolated high-care areas, proper air pressurization or allergen controls or do not have sufficient food safety defense measures in place, due to their construction which began before FSMA regulations.

According to a poll that we took within the Plant Construction Survey this year, food safety was the No. 1 concern for both A&E/C firms and their clients (according to A&E/C firms). Out of more than three dozen trends or concerns, A&E/C firms were asked to rank in order of importance only five trends that were most important to them as design firms, and then what their clients (food and beverage processors) considered key in their own plant designs.

Top 10 A&E/C Hot Trends

- Food safety: FSMA regulations/GFSI (design, layout, etc.)

- Flexibility in plant design to accommodate flexible manufacturing

- Overall cost/ controlling costs

- Fast project deployment

- Old plant vs. build new—Easier to build new than upgrade

- Capital availability

- Raw vs. cooked (RTE) side design

- Automation: process control, robotics, packaging, etc.

- Virtual reality/ augmented reality/3-D facility design tools

- Scheduling equipment arrival to job site

Top 10 Hot Trends A&E/C Firms Say are of Most Concern to Food Processors

- Food safety: FSMA regulations/GFSI (design, layout, etc.)

- Flexibility in plant design to accommodate flexible manufacturing

- Increasing production to meet demand

- Overall cost/ controlling costs

- Capital availability

- Fast project deployment

- Raw vs. cooked (RTE) side design

- Workforce availability (tech staff)

- Automation: process control, robotics, packaging, etc.

- Sustainability (energy, water, etc.)

Food safety, flexibility drive designs

The two tables (“Table 1: A&E/C Hot trends by decreasing order of importance” and “Table 2: Hot trends A&E/C firms say are of most concern to food processors”) agree that food safety and flexibility in plant design are the top-most concerns, followed by increasing production to meet demand and controlling overall construction costs. As will be discussed later, controlling construction costs has become more of a challenge, due to recent governmental changes.

“Consumer demands play a big role in how we design plants,” says Pablo Coronel, CRB director, food processing.

As manufacturers seek to respond to consumer demands, the plant design must be more flexible and allow for timely modification or [the] addition of process lines. Utilities and control systems must be prepared to hold changes, and the floor plan must also be flexible.

Plant flexibility and adaptive reuse are gaining significant momentum, says Jonathan Marshall, Faithful+Gould vice president, manufacturing sector lead. According to Marshall, research from the Industrial Asset Management Council/Society Industrial Offices Realtors and the Construction Industry Institute says that the locations of food plants will gravitate to larger population centers as the trade-off between the size of the labor pool to higher technological skill sets (Table 2) continues to evolve. The aim is to make plants more flexible, so they have a longer overall production life, while bringing fresh food to populated areas, which reduces transportation costs and increases access to a wider, skilled employment base.

Marshall notes that to meet these needs, buildings will have to be designed:

- For future expansion with open floor plans and building envelope flexibility

- To be scaled up or down through modularization

- Modularly for the easy installation and removal of components, as well as process/packaging and material handling equipment

- To a standard platform and linked through company-wide automation programs and remote monitoring for processing and maintenance

- For adaptability to future products or building reuse in mind

- For sustainability and reduced lifecycle costs

- For net zero waste and utilities usage with an eye on water usage (electricity and gas are relatively inexpensive when compared to water—of which there is a finite supply in certain areas).

Automation solves, creates problems

One area where automation can help a plant become more efficient is in reducing changeover time and decreasing losses during transition, says Matt Williamson, ADF Engineering process department manager.

“Automation and improving plant efficiency is a trend that we feel is only going to continue growing on many different levels,” says Hansen-Rice’s Elyar.

Whether by improving handling efficiency by introducing robots or using technology to reduce processors’ carbon footprints by reducing energy and water use, technology is providing new opportunities, including addressing the accountability of ingredients and improving food safety.

“Both labor and utility costs are areas that can be greatly reduced through automation, so as those costs increase, the use of automation is becoming more prevalent,” says Nathan Larose, CMC Design-Build director of project development. “Many utilities offer significant incentive programs that can make the ROI for these capital investments more attractive.”

But automation isn’t just a group of robots doing primary and secondary packaging. Automation can help the process itself.

“Driven primarily by a commitment to food safety and FSMA adherence, many manufacturers are moving to adopt a more integrated process controls platform, which is based on [ISA] S88 guidelines and unifies recipe management, the engine interface, operator interface and reporting functions,” says Dan McCreary, Dennis Group principal.

This holistic platform gives operators greater control and more data, which ultimately enables them to deliver a consistent quality product with speedier time to market.

Speaking of holistic integration, CRB’s Coronel says the industry is moving toward integration of facility control with food safety and traceability documentation to comply both with GFSI and 21 CFR Part 11 (electronic recordkeeping). This integration allows better documentation with fewer errors, while also simplifying the workflow for compliance with GFSI and FSMA.

According to Eric Bockmuller, The Austin Company senior director, project planning, owners are also showing more interest in process and building control management, so they can closely monitor varying costs in manufacturing their product and how changes made in the process affect their production cost and volume.

ESI Group’s Michler sees automation of all aspects of processing plants continuing, especially in energy management, packaging and palletizing. Beyond those, Michler sees more processors using third-party logistics providers.

Nevertheless, automation needs to be applied in ways that make sense.

“In all cases, the business case for investment in automation weighs labor savings and process/quality improvements versus the capital cost of the automated solution,” says Haskell’s Perkey.

The tasks and systems that are most often automated are those that employ high-volume, repetitive tasks. Custom or non-repetitive tasks generally don’t make sense to automate. With small and several changing products being made per day in some facilities, automation can be difficult and expensive to implement.

Automation and workforce

“Automation has become increasingly important due to the labor shortage,” says Dale Snyder, CEO of Dean Snyder Construction.

But finding help is a concern at two levels: technicians and line workers. (See Table 2.) While automation can fill jobs on the line that nobody may want, skilled people are needed to set up and maintain automation.

“I think we’re going to see many companies struggle to maintain their workforce without a high turnover rate,” says Stellar’s Allsup.

This is particularly true in more cold and wet environments; it’s hard to find people to perform this work at the wages plants are willing to pay.

“I think many companies are going to arrive at a crossroads where they’ll have to weigh the escalation in wages to retain their workforce with [the] investment in robotics to reduce headcount,” adds Allsup.

In addition, as companies grow, they may adapt by maintaining current staffing and supplementing it with automation and robotics.

“The most important trend that we see everybody discussing is ‘where are we getting labor, and how are we going to do the work we do?’” says Steve Tippmann. “The impact is in design and automation, which is now becoming more affordable under the current climate.”

“One change that we’ve seen as a result of technology and automation is the type of worker that plants need to recruit and retain,” says Hixson’s Follmer.

“Because the human workforce is becoming more difficult to attract to the food processing environment, we are seeing processors put more consideration into worker comfort and amenities.”

– Mark Redmond

Today’s food plant employees have much more to do than push buttons. Instead, they must be adept at managing and troubleshooting technology within the plant and often carry tablets throughout the production space to record and verify conditions and processes. With this change in required personnel education and background, processors should be looking at their facility design and amenities as a key factor in employee attraction and retention. Better facilities can attract better employees, adds Follmer.

How do you get better facilities? Design them accordingly is the simple answer.

“Because the human workforce is becoming more difficult to attract to the food processing environment, we are seeing processors put more consideration into worker comfort and amenities,” says Mark Redmond, Food Plant Engineering president.

For example, breakroom spaces are getting upgraded; internet access and natural light are also considerations. Processors are providing spaces for employees to socialize. The food environment is still critical, but spaces for employee comfort are becoming more important than in the past.

Some processors have a mandate to improve employee welfare, says Tyler Cundiff, Gray Construction, vice president, business development, food and beverage. Employee welfare strategies include workspace amenities, reduced travel distances, break area enhancements, “daylighting” and environmental surroundings.

Financial climate: A mixed bag

It would seem that with the recent federal tax cut program, there might be plenty of money available for just about any project.

“I expect to see increased capital spending on projects due to incentives in the Tax Cuts and Jobs Act of 2017 that encourage capital expenditure [CAPEX] spending,” says Stellar’s Allsup.

“In the past, a company would have to write off those investments over seven to 22 years. However, the new legislation provides an immediate write-off for this spending, which goes through 2022, per my understanding,” adds Allsup. “I think we’re going to see a lot of this spending continue, especially given the current environment of widespread mergers and acquisitions. Companies are trying to leverage that incentive to gain market share.”

But M&As can put a crimp on new projects.

“In the past few years, there has been a significant amount of M&A activity among the major food and beverage companies,” says Jens Ebert, PE, PMP, SSOE.

This has typically reduced the capital plan value of firms that are preparing for, or adjusting to, M&A deals. However, these deals have also resulted in numerous network optimization projects intended to take advantage of synergies and eliminate operations that no longer fit the portfolio for some reason, adds Ebert.

“Our firm has been doing a lot of work for our clients to relocate production assets between plants,” he says. “Finally, it’s too early to say, but the Trump tax cuts were intended to spur capital investment, so we might still experience some increased project activity as a result.”

“We have seen an increase in spending by facilities, in part due to the growing economy, as well as an increased demand for product,” says Mark Galbraith.

Renovating (making more efficient and expanding existing facilities) is the fastest way for a processor to see results vs. building a brand-new facility; hence, Galbraith has seen many expansions.

Consolidation due to M&As in the pet food industry has had some effect on projects, says ADF’s Williamson. But another issue has to do with changing standards. Combustible dust safety compliance improvements have emerged as a major driver of capital wherever bulk solids are handled, due to the new NFPA 652 standard, which strives to protect employees from dust explosions and fires.

Although Hansen-Rice has seen some slowing within the larger food processing companies, there is a lot of confidence within the specialty food companies. Growing consumer demand for products like plant-based foods, organic foods and vegetarian products is driving a younger generation of small food companies to scale up their manufacturing capacity to meet that demand. Some processors are even looking to take the leap away from co-packers and build their own specialty manufacturing operations. Elyar says his company’s project load has been shifting away from conventional dry and box packaged foods, as well as snack food-related processors, to projects supporting healthier, fresh, prepared meal kits and the like.

“New products offering better quality and convenience continue to push capital expansions,” says Harlan VandeZandschulp, president, Gleeson Constructors & Engineers. “Tax cuts seem to have increased capital spending, however, tariffs will be detrimental to capital spending.”

Donald Oberlies, PE, vice president, market leader at Alberici, sees an increased interest by food processors on projects, but capital appropriation requests are very slow in proceeding, and projects continue to slide. There has been a stronger push for aggressive schedules and pinching total capital spend. However, owner expectation of the cost of construction is not keeping pace with the real-world cost.

Austin’s Bockmuller says spending is up, as Austin is seeing more activity in building-related capital projects. But newly anticipated steel tariffs are already affecting steel costs on projects, with 10 to 25 percent increases being seen on various steel products.

Austin’s Dearduff thinks the rise in costs of construction materials will also lead processors to locate in already constructed buildings and renovate or fit them out. Recent consolidations and acquisitions, however, may threaten the new construction market, as capital gets tied up in acquisitions, and CAPEX for new projects gets redirected.

Like Austin, Gray Construction has seen positive growth in capital spending on projects over the past two to three years and innovation both in meeting consumer needs for new products and equipment innovations that has moved projects along. But there is another caveat—besides increased cost of materials due to tariffs—to consider.

“The current political climate, especially related to tax reform, is directly affecting processors’ ability to deploy capital into those desired initiatives,” says Gray’s Cundiff.

Capital spending in the food industry is high, and the construction industry in general is extremely busy with growth across the board in almost all sectors. Food processors need to know that these factors translate to construction cost inflation, as subcontractors become more selective of projects, and material supplies are in high demand, advises Cundiff.

A M King

Stuart Jernigan

704-365-3160

Dean Snyder Construction

Dale Snyder

641-357-2283

Food Plant Engineering, LLC

Mark Redmond, PE

513-619-1306

Hixson Architecture & Engineering

Mike Follmer, RA

513-241-1230

ADF Engineering, Inc.

Matt Williamson

937-847-2700

Dennis Group

Dan McCreary

724-816-8548

Galbraith Pre-Design, Inc.

Mark Galbraith

717-226-5203

Shambaugh & Son, L.P.

Jeff Johns

260-740-1517

Alberici

Donald C. Oberlies, PE

314-733-2341

E.A. Bonelli + Associates, Inc.

Mark Di Gino

510-740-0155

Gleeson Constructors & Engineers LLC

Harlan VandeZandschulp

712-258-9300

SSOE

Sam Thurber, PMP

567-218-2205

Big-D Construction

Forrest McNabb

801-415-6030

Epstein

Noel Abott

312-429-8048

Gray Construction

Tyler Cundiff

859-281-5000

Stellar

Todd Allsup

904-260-2900

CMC Design-Build, Inc.

Nathan Larose

617-328-7899

ESI Group USA

Jack Michler

262-369-3526

Hansen-Rice, Inc.

Rick Elyar

410-977-3782

The Austin Company

Jeff (Jed) Dearduff

815-685-0148

CRB

Pablo Coronel

919-334-7067

Faithful+Gould

Jonathan Marshall

612-656-6104

Haskell

Keith Perkey

678-328-2908

Tippmann Group

Steve Tippmann

260-490-3000